Holden & Partners Quarterly Investment Views: Q3 2019 Outlook

As the current bull market reaches its 10th year, it provides an opportune moment for investors to reflect on the environment they have experienced over the last decade. Since 2008, almost all asset classes, except commodities, have delivered handsome returns. So attractive, in fact, that it is tempting to look back on the market’s rise as trouble-free. The theory of economic cycles and the inevitability of recession, alongside the significant asset price declines that accompany it, are easily overlooked when analysing the period as a whole, and investors could be forgiven for possessing unrealistic expectations of future returns.

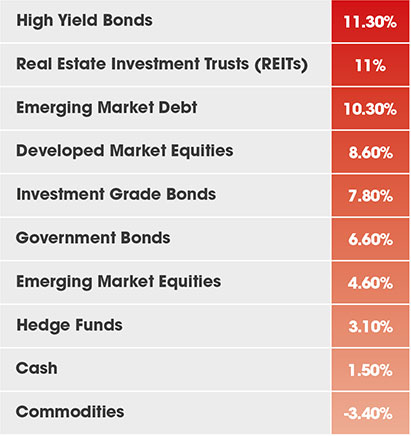

Annualised Asset Class Returns: 2008-20181

But has it really been plain sailing? Whilst this is now one of the longest bull markets in history, it has been accompanied by the shallowest economic recovery in the post-war period. Investor confidence in equity market advances has remained distinctly muted, with the surprise of each new index record high being quickly followed by the anticipation of a correction. Political influence over asset prices and economic growth has also increased to levels not witnessed in several decades, and this has had the effect of creating volatility which is frequently detached from market fundamentals. The development of this bull market may not, therefore, have been straightforward, but it has challenged some widely-held preconceptions of how a ‘normal’ economic expansion should unfold, thereby providing valuable lessons for investors. What are these, and how can they affect the future experiences of clients and asset managers alike?

But has it really been plain sailing? Whilst this is now one of the longest bull markets in history, it has been accompanied by the shallowest economic recovery in the post-war period. Investor confidence in equity market advances has remained distinctly muted, with the surprise of each new index record high being quickly followed by the anticipation of a correction. Political influence over asset prices and economic growth has also increased to levels not witnessed in several decades, and this has had the effect of creating volatility which is frequently detached from market fundamentals. The development of this bull market may not, therefore, have been straightforward, but it has challenged some widely-held preconceptions of how a ‘normal’ economic expansion should unfold, thereby providing valuable lessons for investors. What are these, and how can they affect the future experiences of clients and asset managers alike?

1. Bull markets have no set time limit

The current expansion in history is testament to the adage that ‘bull markets do not die of old age’. The length of an economic cycle is not an indication of its future prospects, nor is the full valuation of a stock market a signal that prices are set to fall. Rather, it takes a negative shock for investors to reappraise their view of the economic outlook and the likely repercussions for markets. There may be several reasons for this: trade tensions, war, or political turmoil, but, often, it takes the form of inappropriate policy from central banks; fearing inflationary pressure and an overheating economy, interest rate rises are used to tighten policy either too soon or too quickly, thereby strangling any remaining, and already weak, growth.

The slow recovery of this cycle has meant that, for the most part, fears of this type of policy misstep have been subdued. Inflation has remained stubbornly low and the lacklustre expansion has meant that there has been little sign of excess. Yet the market reaction to the Federal Reserve’s (the Fed’s) perceived tightening bias in Q4 2018 demonstrated how dramatically it can contribute to market volatility. December represented the worst end to the year for stock markets in the last thirty as economic data weakened and took investors’ expectations and asset valuations with it.

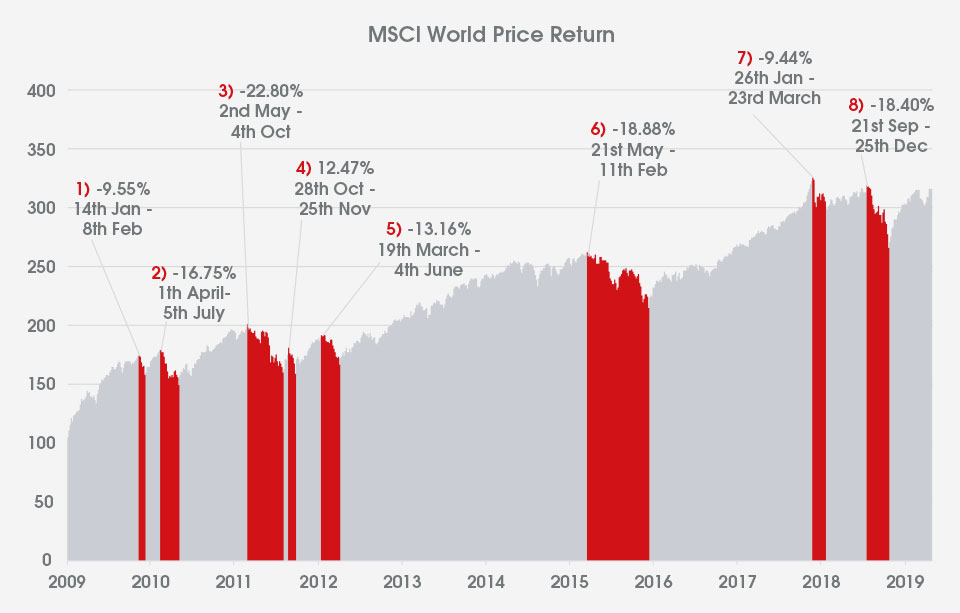

Whilst it is not surprising that, more than a decade on from the financial crisis, recession fears are rising, it does not make one more likely to occur. It is tempting for investors to become increasingly influenced by short-term noise as an expansion ages, questioning whether the global economy may become a victim of slowing growth, political rhetoric, or increasing leverage, all of which exacerbates volatility. Markets rarely rise continuously, but periodic falls, such as that experienced in Q4 2018, often prove to be little more than sentiment-driven corrections (loosely defined as a decline of greater than 10% but less than 20%) followed by a rebound. Such drops are a commonplace feature of bull markets and are not necessarily symptomatic of an approaching bear market: a decline driven by a deterioration in fundamentals, rather than panic. In fact, less than 15% of the market corrections that have occurred since 1980 have signalled a change in the cycle and the start of a downturn2. The current bull market in global equities can be said to have experienced approximately eight corrections and, as the chart below demonstrates, these have all transpired to be simply blips in an upward trend.

This phenomenon, whilst temporarily disruptive, is not without its benefits. Investors’ expectations are revised downwards with each sell-off, adjusting valuations to more realistic levels and reducing the risk of companies disappointing on earnings expectations, leaving the bull with further to run. At Holden & Partners, we maintain our view that a recession is not imminent, although a further deterioration in geopolitical risk would leave the global economy extremely vulnerable. Fundamentally, the Fed’s termination of its rate-hiking cycle in the face of weak growth and persistently low inflation should keep borrowing costs contained, thereby supporting an extension of the cycle through business investment and consumption. At ten years old, this bull market is certainly prolonged, but may not be over just yet…

Source: FE Analytics. Data as of 30th June 2019. Represents MSCI World Price Return (USD) in percentage terms from 09/03/2009 – 30/06/2019, rebased to 100 on 09/03/2009

2. It is not inconceivable that stocks and bonds will move in the same direction and the same time

Traditionally, bonds have played a crucial risk-dampening role in portfolios, providing a steady income with lower levels of volatility than that of equities, thereby offering downside protection and diversification. Fixed interest assets typically experience lower drawdowns than stocks and therefore have the potential to cushion market falls if global growth fails to live up to expectations, or if equity markets are negatively impacted by an external shock. There is also the fundamental issue of safety; the risk of a government or corporation being unable to meet annual interest payments or pay back capital at bond maturity, is generally far lower than that of volatility in a company’s share price.

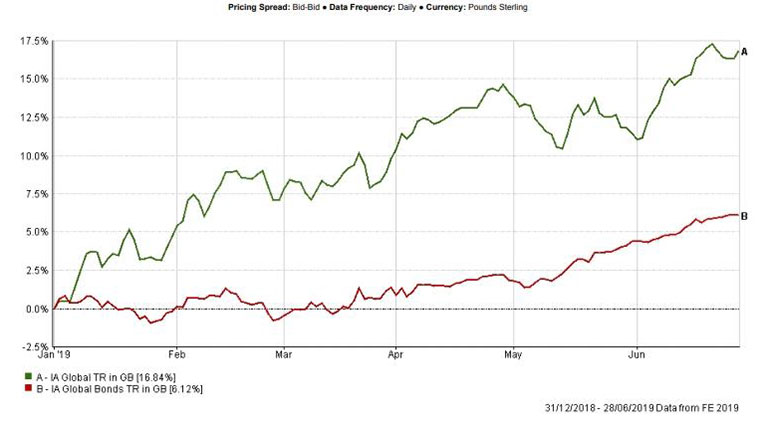

It may, therefore, seem counterintuitive that ‘safe-haven’ securities such as developed-world government bonds, for which demand increases during times of economic stress, have recently rallied in tandem with risk assets – see the chart below. It may be even more confusing considering that the inversion of the US yield curve – a phenomenon whereby long-dated Treasury yields fall below short-term rates – is suggesting that a potential recession will result in a series of interest rate cuts. Yet, there may be a plausible reason for this apparent contradiction in market signals.

Since 2009 investors have become accustomed to, and somewhat reliant on, the policy response to weakening growth; economic data disappoints and central banks step in to support equity markets by lowering interest rates, either directly through rate cuts or indirectly through the purchase of government securities. The result of this is a decline in the global discount rate used to value the cashflows generated by stocks, as well as the available yield on bonds, thereby increasing asset prices of both, despite declining growth expectations. Rather than disregarding the caution implied by a rallying bond market, equity markets are simply pricing the effect of the end to the Fed’s tightening cycle and a return to interest rate cuts.

Geopolitical tensions and a slowdown in growth means that this may continue. The future trajectory for interest rates is likely to be stationary or downwards, thereby removing the pressure of rising rates which rocked markets in late 2018. Low inflation and structural issues, such as technological advancement, which are helping to keep price increases anchored relative to their long-term averages, has afforded central banks the flexibility to maintain rates at current levels. This bull market has therefore represented an environment of lower real equilibrium rates and global returns than of previous cycles, providing the potential for equities and fixed income to move in tandem. Whilst it is historically unusual, the trend need not cause long-term, globally diversified investors alarm.

Source: Guide to the Markets, J.P. Morgan Asset Management. Returns shown are per annum and are calculated based on monthly returns from 1950 to latest. Data as of 30th June 2019.

3. Structural growth drivers, not short-term performance, should form a key part the investment case for an asset

Many market participants continue to concentrate on short-term horizons, relying on earnings forecasts and working with consensus assumptions in pursuit of immediate gain. The collective effect of this is that financial markets may be ill-placed to recognise, and react to, the structural changes which are taking place in the world and which will shape our future.

At Holden & Partners, we have consistently maintained that, as growth around the world becomes harder to come by, companies exhibiting earnings resilience should be rewarded. It can be difficult to make sense of the proliferation of information emanating from markets to determine which assets may best serve our clients’ long-term needs, but it typically involves investment in areas which can deliver strong underlying growth and identify opportunities and risks that may be underappreciated by the market. Identifying societal challenges, changing consumer preferences, opportunities for disruption, and analysing how a business may capitalise upon them to generate a sustainable business advantage is crucial to this process. It provides our portfolios with an inherent quality bias which we believe will lead to outperformance in the current market environment.

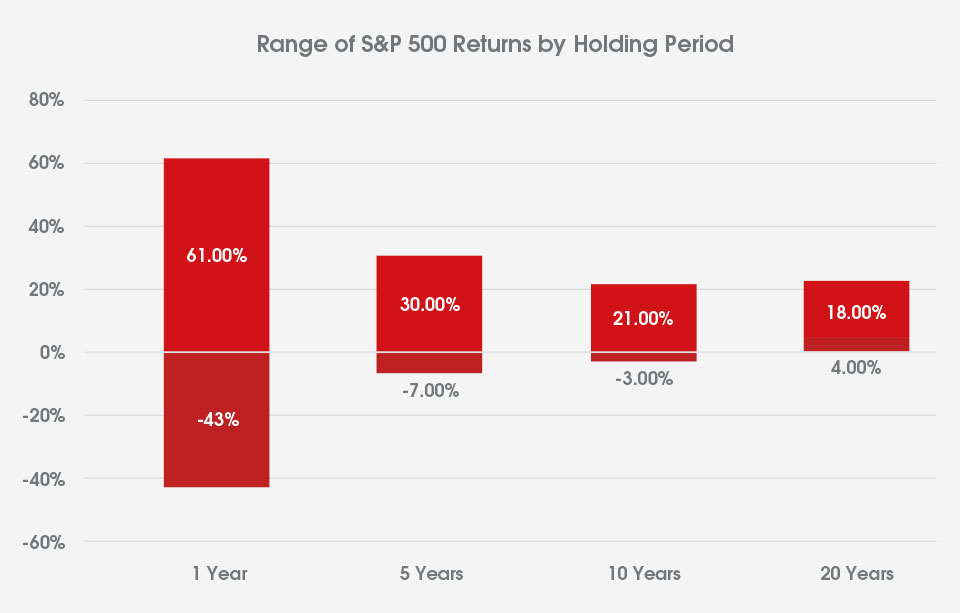

It is worth reiterating the importance of maintaining a long-term view, possessing a diversified portfolio, and using episodes of volatility to take advantage of any attractive opportunities it may present. As the chart below demonstrates, clients who remain invested in accordance with their financial plan are better placed to meet their long-term goals and achieve the appropriate inflation-linked returns over time. Shifting portfolio allocations based on temporary instability can result in a far wider, and more uncertain, distribution of outcomes, thereby destroying value for asset owners. The time spent invested in the market, particularly over a 10-year bull market, will always be far more important than the initial timing of it and continues to serve investors well.

Source: Guide to the Markets, J.P. Morgan Asset Management. Returns shown are per annum and are calculated based on monthly returns from 1950 to latest. Data as of 30th June 2019.